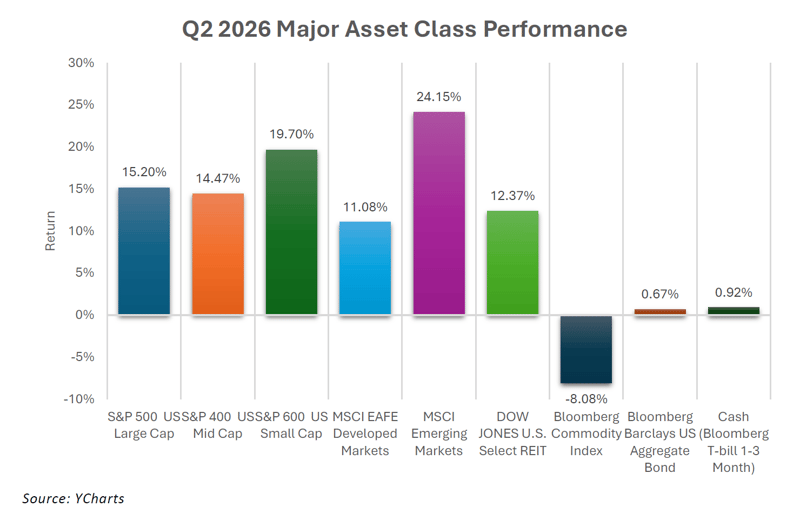

- The second quarter delivered one of the sharpest V-shaped recoveries in recent market history. The S&P 500 gained 15.2% and the Nasdaq-100 posted its second-best quarter in 25 years, as fears that gripped markets during the first quarter's selloff gave way to conviction.

- Leadership broadened well beyond mega-cap technology. The S&P 600 small-cap index rose 19.7%, the MSCI Emerging Markets surged 24.2%, and six of the nine major asset classes posted double-digit returns. Client portfolios outperformed during the quarter, aided by our overweight to US mid- and small-caps, international equities, and a significant underweight to commodities.

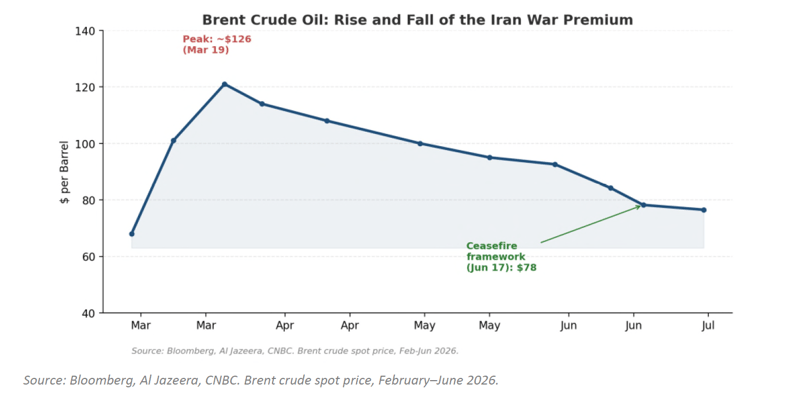

- A ceasefire framework de-escalated the Iran conflict and eased the blockade on the Strait of Hormuz. Brent crude fell nearly 40% from its March peak and commodities as an asset class fell 8.1%.

- New Federal Reserve Chair Kevin Warsh took office in May and struck a surprisingly hawkish tone on inflation that pushed Treasury yields higher and kept bond returns in check.

Market Returns

Equity markets staged one of their sharpest quarterly reversals in recent memory, easing the anxiety that defined the first quarter. The S&P 500, which had fallen 4.3% in the opening months of the year amid the outbreak of the Iran War and a wave of artificial intelligence-related selling, rallied 15.2% in the second quarter — its best quarterly showing since the post-pandemic rebound in 2020. The Nasdaq-

100 climbed further still, turning in its second-best quarter in 25 years as investors gained conviction in the durability of the AI investment cycle.

The second quarter rally was broad-based and characterized by widespread strength across many asset classes. US equities posted mid-to-high teen returns across the capitalization spectrum, from large-cap to small-cap. International markets told a more uneven story. Developed international equities, as measured by MSCI EAFE, advanced a solid 11.1%. Emerging markets were the standout performer of the quarter, gaining 24.2% on the strength of extraordinary rallies in South Korea and Taiwan, whose chipheavy markets sit at the center of the AI buildout — a theme examined in more detail below.

Commodities were the lone asset class in the red, falling 8.1%. Oil prices retreated sharply on progress toward de-escalation in the Middle East. Bonds, as measured by the Bloomberg Barclays US Aggregate Bond Index, eked out a modest 0.67% gain, held in check by rising Treasury yields tied to a more hawkish Federal Reserve.

Client model portfolios performed admirably in the second quarter. Our overweight to US mid- and small-caps and international equities and our zero weight to commodities delivered significant relative outperformance.

The Iran War De-Escalates and Oil Prices Come Back to Earth

The single largest swing factor for markets this quarter was the gradual de-escalation of the Iran conflict that has dominated headlines since late February. After Brent crude oil spiked above $126 per barrel in March following the closure of the Strait of Hormuz, prices began a steady retreat as the US and Iran worked through a series of ceasefire extensions and a broader memorandum of understanding. By late June, Brent had fallen to the high-$70s, down nearly 40% from its wartime peak.

The retreat in energy prices had consequences well beyond the commodities market. Falling gasoline prices helped stabilize consumer sentiment, lower input costs eased margin pressure across a wide swath of industries, and receding energy-driven inflation fears removed one of the key overhangs on equities from the first quarter. That said, tanker traffic has been slow to normalize given war-related damage to regional infrastructure and periodic flare-ups are a reminder that we are experiencing deescalation, not a resolution. The trajectory is viewed as a net positive heading into the second half of the year.

The Broadening AI Trade

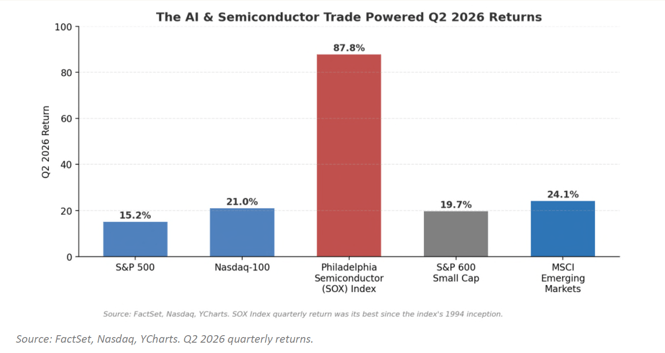

The first quarter was defined by investor skepticism toward AI capital spending. The second quarter flipped that skepticism on its head. Corporate earnings season was decidedly strong — roughly 85% of S&P 500 companies beat earnings estimates — and NVIDIA's blowout May report (revenue of $81.6 billion, up 85% year-over-year, with data-center revenue nearly doubling) reaffirmed that demand for AI infrastructure remains, in management's own words, "parabolic." That confirmation fueled a powerful rally in technology and semiconductor stocks that carried markets to record highs. As illustrated in the chart below, the popular semiconductor index SOX returned an eye-watering 87.8% in the quarter.

What also stood out is just how global this AI cycle has become. Emerging markets returned 24.2% in the quarter due mostly to South Korea and Taiwan whose markets are highly concentrated in memorychip and semiconductor-foundry companies supplying the global AI buildout. Korea's market climbed more than 75% for the quarter and Taiwan's gained 48%. Samsung, SK Hynix, and Taiwan Semiconductor Manufacturing rode surging demand for the advanced chips to tremendous gains.

A New Fed Chair Brings a Hawkish Tilt

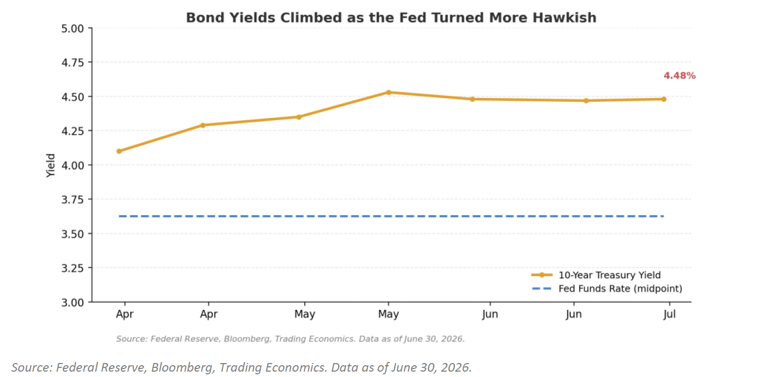

The second quarter also marked a historic transition at the Federal Reserve. Kevin Warsh was confirmed and took office as Fed Chair in May succeeding Jerome Powell whose term concluded after years of pressure from the Trump administration over the pace of rate cuts. Markets initially expected Warsh, who had campaigned for the role on a more dovish platform, to move quickly to lower rates. Instead, in his first meeting as chair, Warsh held rates steady at 3.50%–3.75% and delivered a notably hawkish message, stating plainly that the Fed had "missed on inflation for five years" and that anyone expecting the Fed to tolerate inflation above its target of 2% “would be disappointed”. Nine of eighteen FOMC

participants penciled in at least one rate hike for 2026, a sharp reversal from prior projections.

The energy price shock discussed earlier in this letter was the primary catalyst of Warsh’s hawkish stance. Core inflation climbed to 3.4% in the spring, its highest level in roughly three years. Treasury yields moved higher across the curve in response: the 10-year yield rose from 4.1% at the end of the first quarter to near 4.5%, and the 30-year touched 5.19% in the spring, its highest level since 2007. The move also completed a historic shift in the shape of the yield curve — after a 27-month inversion, the longest on record, the 10-year/2-year spread turned positive in April. This movement in the yield curve and overall increase in yields put downward pressure on bonds during the quarter. The index returned

just 0.67%.

Encouragingly, Warsh noted that cooling energy costs should offer the clearest near-term path toward the rate relief markets are still hoping for. Current fixed income positioning remains well suited for that trajectory.

Outlook and Portfolio Changes

We enter the second half of 2026 with optimism. Markets absorbed a geopolitical shock, a leadership transition at the world's most important central bank, and renewed inflation concerns yet still delivered one of the strongest quarterly rallies in years. Corporate earnings grew at their fastest pace since 2021, jobs growth remains resilient, financial conditions remain attractive, and the AI buildout is alive and

well.

Given the strength of the rally, the second quarter presented an ideal window to rebalance client portfolios. Equity allocations had drifted meaningfully above target in many accounts as stocks surged. Positions were trimmed back closer to target weights in a tax-efficient manner and proceeds were redeployed into fixed income and other underweight areas. Rebalancing after a rally of this magnitude is one of the more valuable, if less exciting, tools available for keeping portfolio risk aligned with long-term goals rather than short-term momentum.

While optimistic, we remain aware of downside risks. Valuations are higher than average, tensions in Iran are far from settled, and bouts of volatility should be expected as investors periodically reassess the pace of AI-related capital spending against realized returns. Chair Warsh's hawkish debut is a reminder that the path of interest rates is unlikely to be linear either. The nonlinear nature of markets underscores the value of staying diversified, disciplined, and appropriately positioned across asset classes, which is exactly the approach that allowed our portfolios to weather the first quarter's volatility and participate in the second quarter's recovery.

Thank you for your trust. Please don't hesitate to reach out with any questions as the second half of the

year unfolds.

Kyle Matthews, CFA on behalf of Miller Financial Services and OnePoint BFG Wealth Partners

DISCLAIMER

Investment advisory and financial planning services offered through Bleakley Financial Group, LLC, an SEC registered investment adviser, doing business as OnePoint BFG Wealth Partners and Miller Financial Services.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. The market and economic data is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The information in this report has been prepared from data believed to be reliable, but no representation is being made as to its accuracy and completeness.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Nothing in this material should be construed as investment advice offered by OnePoint BFG Wealth Partners or Miller Financial Services. This market update is for informational purposes only and is not meant to constitute a recommendation of any particular investment, security, portfolio of securities, transaction or investment strategy. No chart, graph, or other figure provided should be used to determine which securities to buy, sell or hold. No representation is made concerning the appropriateness of any particular investment, security, portfolio of securities, transaction or investment strategy. You should speak with your own financial professional before making any investment decisions.

Past performance is not indicative of future results. Neither OnePoint BFG Wealth Partners nor Miller Financial Services guarantee any specific outcome or profit. These disclosures cannot and do not list every conceivable factor that may affect the results of any investment or investment strategy. Risks will arise, and an investor must be willing and able to accept those risks, including the loss of principal.

Certain statements contained herein are statements of future expectations and other forward-looking statements that are based on opinions and assumptions that involve known and unknown risks and uncertainties that would cause actual results, performance or events to differ materially from those expressed or implied in such statements.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful. The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings. International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets. The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings.

OnePoint BFG Wealth Partners (“OnePoint BFG”) often uses Artificial Intelligence (“AI”) in the generation of reports such as the above. OnePoint BFG and its employees are bound by all applicable Firm policies and procedures when using AI. AI is subject to risks and limitations. OnePoint BFG has established policies and procedures to ensure all AI generated material goes through human review prior to dissemination. For additional information regarding AI, please refer to OnePoint BFG’s ADV 2A.

OP 26-0750