- A market rotation in the first quarter saw mid and small caps, value, and commodities lead and mega-cap technology stocks lag. Market narrative shifted throughout the period from worries about the impacts of artificial intelligence to the Iran War and oil price shocks.

- The US and Israel launched their first attacks on Iran on February 28th, sending global geopolitical order into a tailspin. The war has led to a surge in commodity prices and an increase in inflation expectations.

- Potential knock-on effects of artificial intelligence caused a selloff in AI hyperscalers, software companies, and a wide-ranging basket of companies thought to be in jeopardy of replacement. We believe investors are taking a sell now, ask questions later approach and that the odds of AI boosting labor productivity and corporate earnings are greater than the odds of AI replacing entire swaths of industry.

Market Returns

Equity markets generally pulled back to start the year after posting a strong 2025. A rotation in the first quarter saw mid and small caps, value, and commodities lead while mega-cap technology and international lagged. The broad market narrative shifted quickly in the quarter from a focus on artificial intelligence (AI) and software-related pressures to the Iran War and oil price shocks.

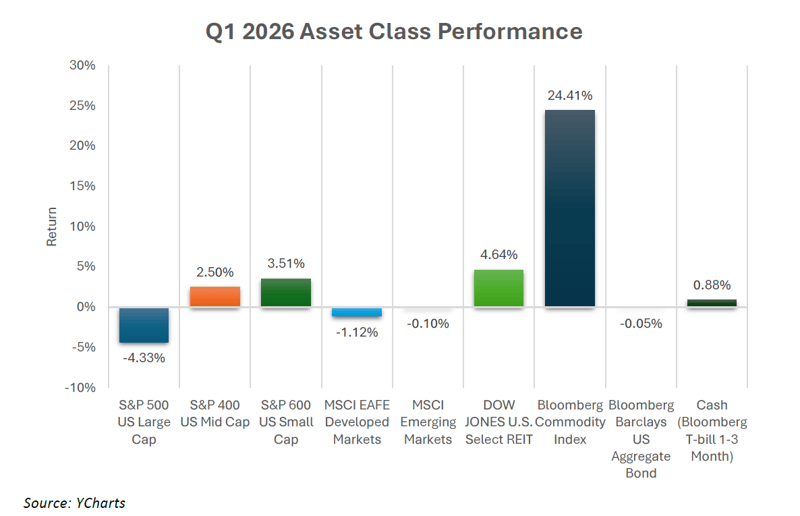

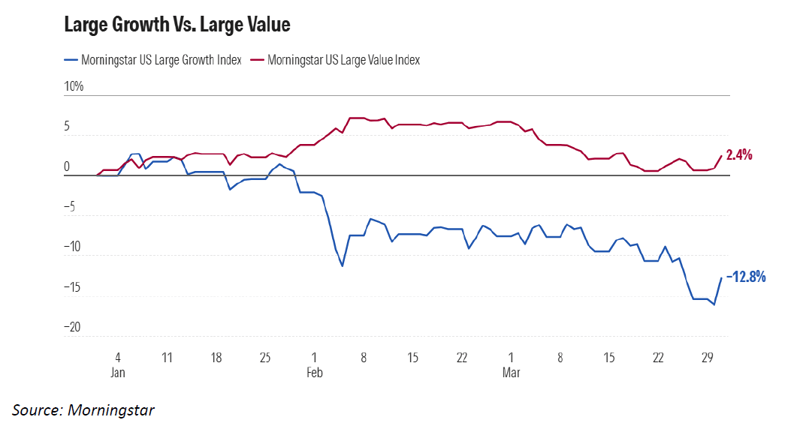

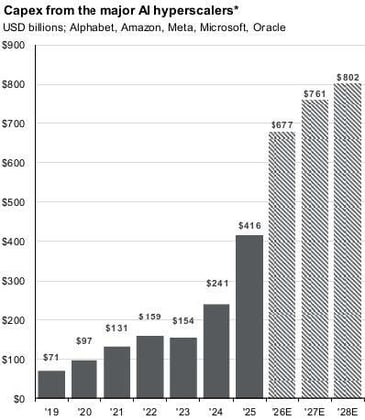

The equity market rotation was one delineated by market cap, style, and sector. The S&P 500 fell 4.3% while US mid-cap rose 2.5% and US small-cap returned 3.5%. The S&P 500 struggled with a retracement in mega-cap tech names amid growing scrutiny around the payoff from enormous artificial intelligence capital expenditures (capex). There was a massive divergence in growth and value styles. Morningstar US Large Growth Index finished the quarter -12.8% while US Large Value Index was up 2.4%. It was US Large Growth’s worst quarterly performance since the secondar quarter of 2022 when it sold off a staggering 29.8%.

Mid cap and small cap outperformance benefited from the shift away from richly valued mega-cap tech into smaller, domestically focused companies with more attractive valuations. We remain overweight US mid and small cap.

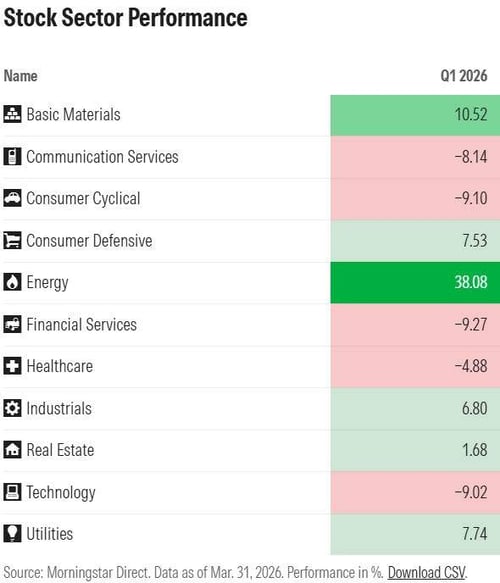

US equity sector performance varied greatly. Energy stocks benefited from the runup in oil, natural gas, and gasoline prices. Basic Materials and Utilities also posted strong returns while Consumer Cyclical and Technology were each down over 9%. Software and semiconductors sold off during the quarter on concerns that advancements in generative AI will disrupt traditional software-as-a-service (SaaS) business models. We believe those fears to be overdone and dive further into this dynamic later in the commentary.

International developed equities were down 1.1% and emerging markets were essentially flat at -0.1%, serving as a good diversifier to US large cap. Despite geopolitical uncertainty and inflationary fears, international markets outperformed the S&P 500 due mainly to the aforementioned rotation out of mega-cap tech stocks.

Commodities were the far and away leader during the period as raw material prices soared due to the Iran War and closure of the Strait of Hormuz. Brent crude oil peaked at a four-year high of $117 per barrel in mid-March, representing a 92% jump from an early January low. Natural gas and gasoline prices also rose dramatically.

Bonds, as measured by the Bloomberg Barclays US Aggregate Bond Index, were flat on the quarter after digesting a runup in yields which I discuss in more detail below.

Our model portfolios held up well in the quarter and provided downside protection for clients in a volatile time in markets.

Iran War

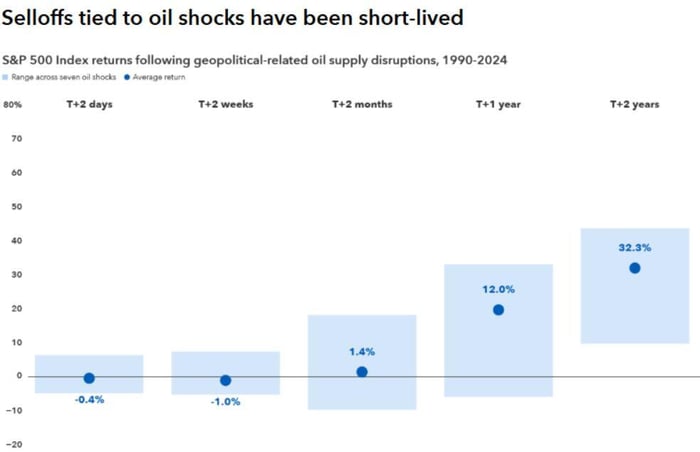

The US and Israel launched their first attacks on Iran on February 28. Investors initially thought the conflict would be brief but the war continues on (although a temporary ceasefire agreement was just reached as of this writing). The Strait of Hormuz became a choke point for 20% of the world’s oil, sending prices skyward and stoking inflationary fears. There have been immediate inflationary impacts like prices at the pump and higher shipping costs and longer-term impacts such as higher food prices and higher energy production costs out of the Middle East. Capital Group offered interesting forward return statistics stating that selloffs due to oil shocks are usually short-lived (see below). S&P 500 returns are strong on average starting 2 months after the initial shock and persisting from there. We present this information as a historical case study but this time may very well be different.

Source: Capital Group

The Federal Reserve noted that progress towards their 2% inflation mandate may be slower than previously forecast due to the conflict. The central bank is taking a wait-and-see approach to better gauge the economic impact from the war. Major banks Goldman Sachs and JP Morgan notched their inflation expectations higher, as did many others on Wall Street. That caused a tough environment for bonds.

Bond Market

With widespread expectations for a pickup in inflation, bond yields soared. The 10 Year Treasury yield had fallen to its lowest level in 18 months in late February, right before Operation Epic Fury. The conflict and ensuing rise in oil prices caused the 10-year to increase from below 4.0% to a high of 4.4%. The 2-year experienced a similar jump from a low of 3.40% to 3.79%.

The US Aggregate Bond Index held up well amidst this rising yield environment. Short-term bonds eked out small gains while longer-duration and credit-sensitive segments of the bond market posted modest declines. We continue to view the setup for bonds as appealing, with attractive carry available from high current yields.

Source: Morningstar, Federal Reserve Economic Database

Artificial Intelligence

Investor fears over AI surfaced in a multipronged fashion in the quarter over replacement and revenue concerns. AI replacement fears are based on the threat of AI replacing or displacing entire industries and segments of the economy. AI revenue related fears involve investors calling into question the level of software and hyperscaler capex and whether it would quickly result in durable revenue growth – essentially will AI investment result in revenue and profit.

We think investors are selling based on these fears before stopping to contemplate long-term effects of AI. Both AI development and adoption are still in the early stages. Regarding adoption, the Census Business Trends and Outlook Survey stated that only 19% of US businesses are using AI in any business function as of March 2026.

We believe the odds of AI being used as a tool to boost labor productivity and corporate earnings are higher than the odds of AI replacing entire swaths of industry. Structural tailwinds of rising enterprise demand, improving infrastructure cost curves, and increasing multiyear capex commitments should fuel further growth and the opportunity for clients to compound wealth in AI-related verticals remains intact. In the event an AI selloff or broader equity market selloff occurs, we have structured client portfolios to withstand five years of volatility without having to sell from equity positions.

Source: Bloomberg, JP Morgan Asset Management

Outlook

Markets experienced a healthy re-rating and broadening out in the first quarter. Diversification was rewarded in the quarter and we believe further broadening will occur throughout the remainder of the year.

We trimmed equities back to target in December of 2025 and will look for opportunities to rebalance portfolios to target again in the near future. We have already incorporated tax-aware strategies where appropriate and have increased allocations to actively-managed ETFs given their lower expense ratios and tax efficiency relative to traditional mutual funds.

In the management of client capital, we constantly stive to cut through the noise, build resilient portfolios designed to withstand market volatility, and act only on information that has the potential to deliver impactful long-term results.

Please reach out with questions or if you would like to discuss your portfolio.

Kyle Matthews, CFA on behalf of Miller Financial Services and OnePoint BFG Wealth Partners

DISCLAIMER

Investment advisory and financial planning services offered through Bleakley Financial Group, LLC, an SEC registered investment adviser, doing business as OnePoint BFG Wealth Partners and Miller Financial Services.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. The market and economic data is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The information in this report has been prepared from data believed to be reliable, but no representation is being made as to its accuracy and completeness.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Nothing in this material should be construed as investment advice offered by OnePoint BFG Wealth Partners or Miller Financial Services. This market update is for informational purposes only and is not meant to constitute a recommendation of any particular investment, security, portfolio of securities, transaction or investment strategy. No chart, graph, or other figure provided should be used to determine which securities to buy, sell or hold. No representation is made concerning the appropriateness of any particular investment, security, portfolio of securities, transaction or investment strategy. You should speak with your own financial professional before making any investment decisions.

Past performance is not indicative of future results. Neither OnePoint BFG Wealth Partners nor Miller Financial Services guarantee any specific outcome or profit. These disclosures cannot and do not list every conceivable factor that may affect the results of any investment or investment strategy. Risks will arise, and an investor must be willing and able to accept those risks, including the loss of principal.

Certain statements contained herein are statements of future expectations and other forward-looking statements that are based on opinions and assumptions that involve known and unknown risks and uncertainties that would cause actual results, performance or events to differ materially from those expressed or implied in such statements.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful. The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings. International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets. The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings.

OP# 26-0379