The Federal Reserve occupies a central position in the U.S. economy and financial markets, and its influence has expanded considerably over recent decades. From the 2008 global financial crisis to the inflationary pressures of recent years, investors have scrutinized every Fed decision closely. Leadership changes at the Fed, therefore, naturally draw significant attention from investors and the public alike.

Kevin Warsh, confirmed by the Senate as the new Fed Chair, brings considerable experience as a former member of the Fed's Board of Governors during the global financial crisis.1

Markets have responded positively to his appointment, recognizing him as a familiar figure with deep knowledge of monetary policy. Understanding what his leadership may mean for Fed policy and investor portfolios is an important consideration going forward.

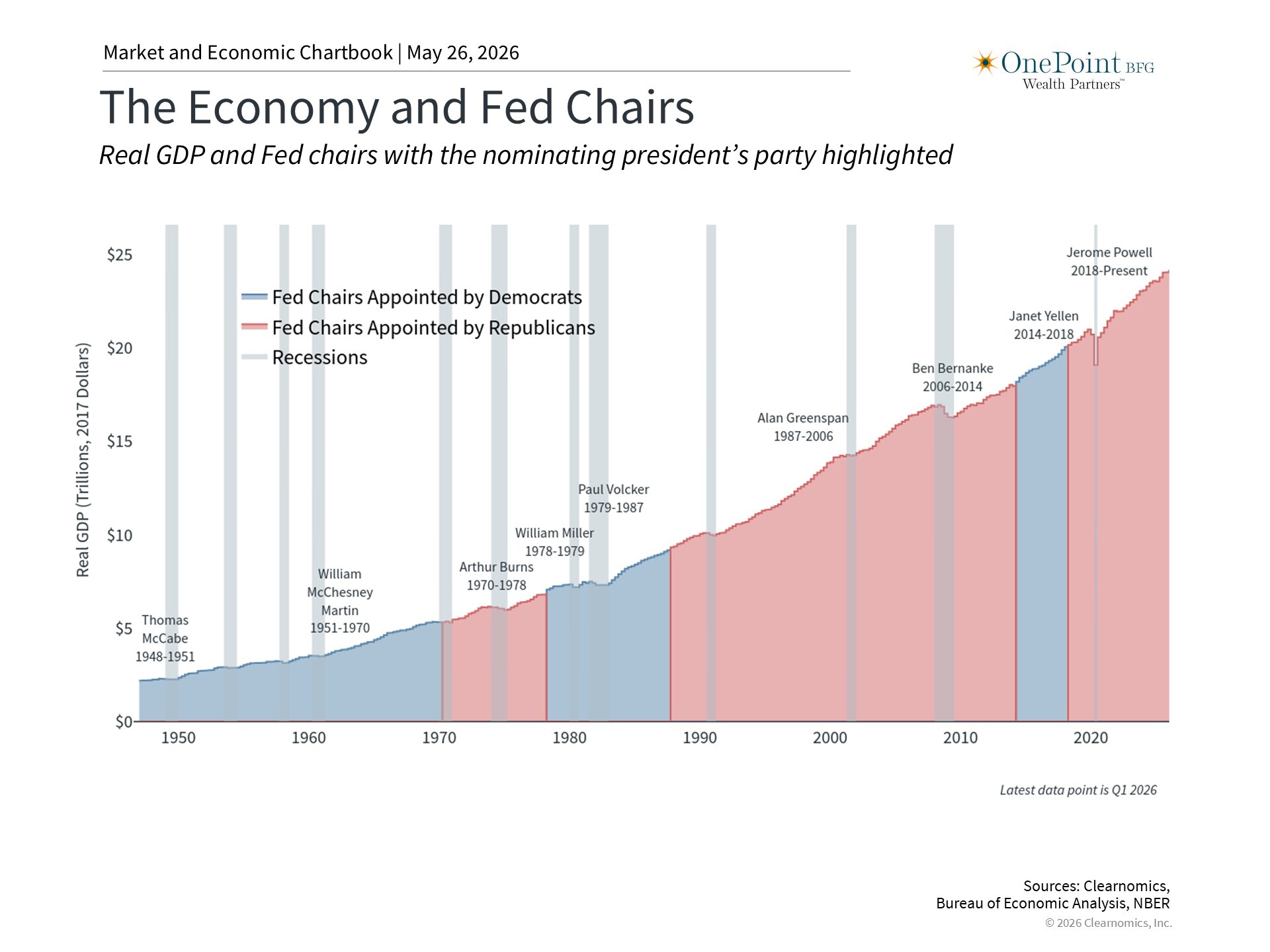

The economy has grown under many Fed leaders

Taking a broad historical view of Fed leadership offers useful perspective. The Fed Chair serves a four-year term, while Board of Governors members serve staggered 14-year terms, a structure designed to insulate monetary and regulatory decisions from political pressures. This principle, known as "Fed independence," has been debated and tested throughout history.

As the accompanying chart illustrates, the U.S. economy has expanded across the tenures of multiple Fed chairs, regardless of the administrations that nominated them. Each leader, from Paul Volcker to Jerome Powell, navigated distinct economic challenges, including stagflation, the global financial crisis, the pandemic, and the recent inflation surge. Throughout these periods, the Fed adapted its tools to evolving circumstances.

It is worth noting that the Fed and interest rates represent only one part of the broader economic picture. The Federal Reserve Reform Act of 1977 established a "dual mandate" to promote maximum employment and stable prices. Even so, many of the Fed's tools, such as the federal funds rate, work with what economists describe as "long and variable lags," and the central bank cannot directly control economic forces such as energy prices or the labor market effects of technological change.

Kevin Warsh favors a more focused approach to central banking

In his Senate testimony, Warsh expressed support for "a clearer, cleaner match between the Fed's powers and responsibilities," indicating a preference for a more narrowly focused central bank.2

He also stressed that "monetary policy independence is essential" and that policymakers must act in the national interest. Historically, Warsh has been characterized as an "inflation hawk," meaning he tends to favor higher interest rates as a safeguard against rising inflation, along with institutional reform at the Fed.

There are several investing implications worth considering. First, it remains to be seen how Warsh's views will translate into policy, particularly given the current inflationary environment and any tension with the White House's preference for lower rates. Headline CPI stood at 3.8% year-over-year as of April 2026, with core CPI at 2.8%, both above the Fed's 2% target, partly reflecting higher oil and gasoline prices driven by the war in Iran. Conflicts between the executive branch and the Fed are not new; they have occurred under multiple administrations throughout history, even when the president appointed the sitting Fed Chair.

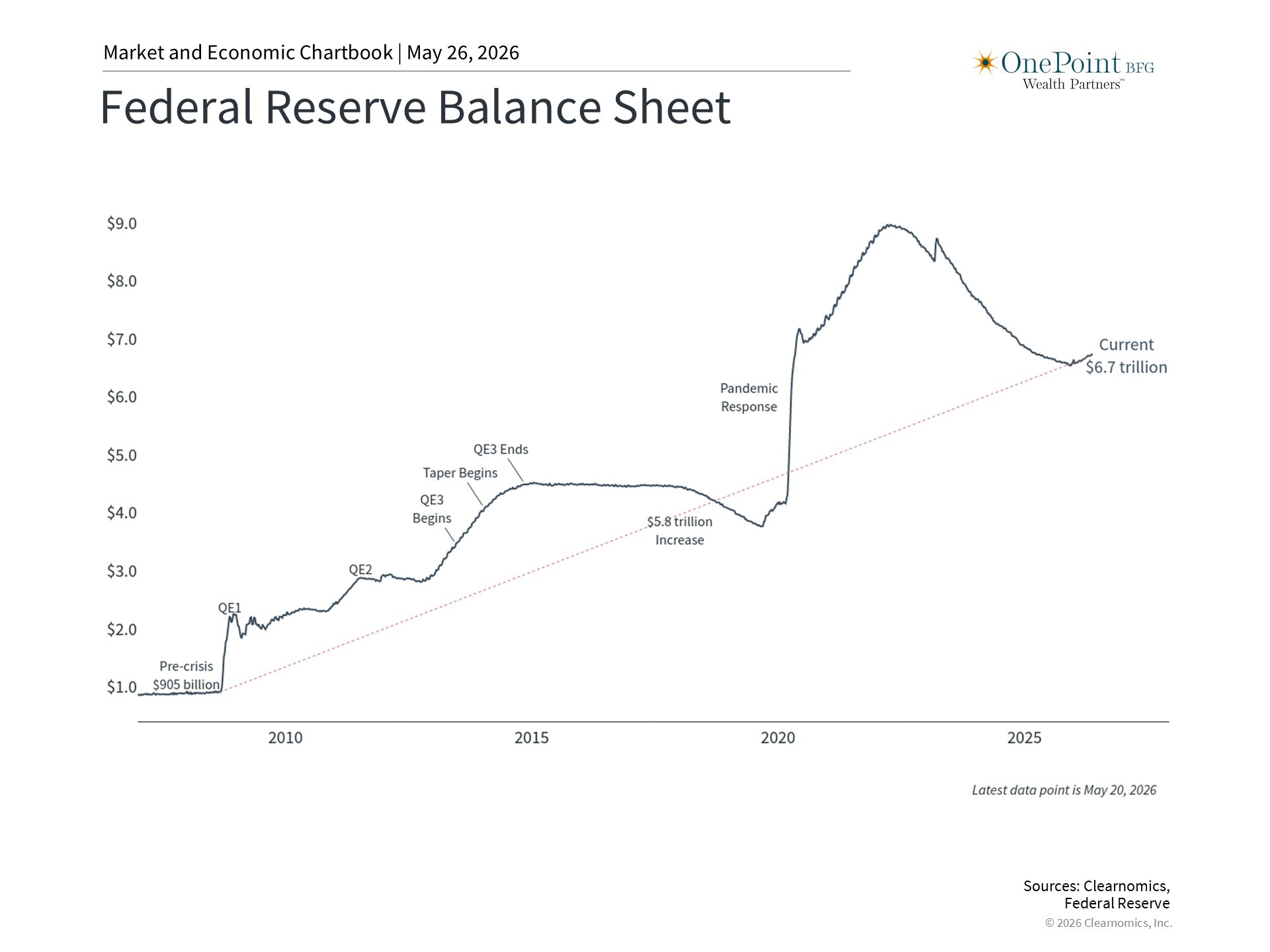

Second, while Warsh has criticized the Fed's involvement in green initiatives and social policy, he has not called for dismantling the institution's core functions. He has acknowledged that crisis-era balance sheet expansion was appropriate, given his direct involvement in those decisions.3

However, he believes the Fed should "retrace its steps" once conditions normalize. With the Fed's balance sheet still sizeable at $6.7 trillion, further "quantitative tightening" could affect bond prices, mortgage rates, and corporate borrowing costs.

Third, Warsh has argued that Fed policy since the pandemic has contributed to growth in the federal deficit and national debt, and that while spending may be warranted during recessions, monetary policymakers should avoid fiscal commentary and ensure such measures are symmetric.4

While the Fed does not directly control federal spending, its guidance and rate decisions can indirectly influence borrowing costs and fiscal conditions.

Inflation and monetary policy create a complex backdrop for the new Fed Chair

Warsh inherits a challenging policy environment. Fed funds futures now reflect the possibility of a rate increase by early 2027, a notable shift from earlier expectations of further rate cuts. These market expectations shift frequently with new economic data and global developments, so they should be interpreted with caution. Still, they underscore the uncertain path ahead for monetary policy.

For investors, the most important takeaway is that markets and the economy have performed well across many different Fed leadership transitions and policy environments. While changes at the top of the Fed generate uncertainty, they rarely alter the long-term fundamentals that drive financial markets. Earnings growth, productivity, demographics, and innovation remain the most important drivers of long-run returns. Maintaining a long-term perspective, rather than reacting to each policy development, continues to be the most constructive approach.

The bottom line? As Kevin Warsh takes over as Fed Chair, it's important to maintain perspective on the role of the Fed. Ultimately, understanding the longer-term drivers of the market and economy is the best way to achieve financial goals.

References

1.https://www.senate.gov/legislative/LIS/roll_call_votes/vote1192/vote_119_2_00120.htm

2. https://www.banking.senate.gov/imo/media/doc/warsh_testimony_4-21-26.pdf

3. https://www.wsj.com/opinion/the-high-cost-of-the-feds-mission-creep-role-responsibility-monetary-policy-economy-20a352f8

4. Ibid.

Investment advisory and financial planning services offered through Bleakley Financial Group, LLC, an SEC registered investment adviser, doing business as OnePoint BFG Wealth Partners (herein referred to as “OnePoint BFG”).

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. The market and economic data is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The information in this report has been prepared from data believed to be reliable, but no representation is being made as to its accuracy and completeness.

This commentary is for informational purposes only and is not meant to constitute a recommendation of any particular investment, security, portfolio of securities, transaction or investment strategy. No chart, graph, or other figure provided should be used to determine which securities to buy, sell or hold. No representation is made concerning the appropriateness of any particular investment, security, portfolio of securities, transaction or investment strategy. You should speak with your own financial professional before making any investment decisions.

Past performance is not indicative of future results. OnePoint BFG does not guarantee any specific outcome or profit. These disclosures cannot and do not list every conceivable factor that may affect the results of any investment or investment strategy. Risks will arise, and an investor must be willing and able to accept those risks, including the loss of principal.

Certain statements contained herein are statements of future expectations and other forward looking statements that are based on opinions and assumptions that involve known and unknown risks and uncertainties that would cause actual results, performance or events to differ materially from those expressed or implied in such statements.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful. The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings. International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets. The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings.

Advisors associated with OnePoint BFG may be: (1) registered representatives with, and securities offered through Purshe Kaplan Sterling Investments (“PKS”), Member FINRA/SIPC, (2) registered representatives with, and securities offered through PKS, Member FINRA/SIPC and investment advisor representatives of OnePoint BFG; or (3) solely investment advisor representatives of OnePoint BFG, and not affiliated with PKS. Investment advice offered through OnePoint BFG, a registered investment advisor and separate entity from PKS.

OnePoint BFG Wealth Partners (“OnePoint BFG”) often uses Artificial Intelligence (“AI”) in the generation of reports such as the above. OnePoint BFG and its employees are bound by all applicable Firm policies and procedures when using AI. AI is subject to risks and limitations. OnePoint BFG has established policies and procedures to ensure all AI generated material goes through human review prior to dissemination. For additional information regarding AI, please refer to One Point BFG’s ADV 2A.

Copyright (c) 2026 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company's stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

OP 26-0528

.jpg?width=352&name=Shutterstock_2116756223%20(3).jpg)